P>Music, at least for the most part, everyone has made it in, so thank you guys very much for joining us today. This is Scarborough University here doing a webinar on duty drawback. There have also been a lot of changes coming down the pipe in the last six months or so. So before we get in, before we begin here, I'm just a quick little commercial on Scarborough. Scarborough is a group of companies, and we are a US licensed customs broker and freight forwarder. Most recently, we opened a consulting division. Today, with me, I have Pat Caulfield from Grunfeld Desiderio Leibowitz Silverman and Clayshot. Pat and I go back a few years. We've played golf a few times together and know each other from a few events. He is a great attorney, and I think you guys are going to have good insight into some of the things about drawback. We will try to keep the PowerPoint side of this presentation down to about 20 minutes or so, and then we'll spend the rest of the time going through and answering questions. If you guys have questions, I know we've gotten a big chunk of them already. There is a Q&A option in your log in as well, so please feel free to ask them. We will do our best to answer everything live. If we do run out of time, we will get every question answered that we do have. So without that, thanks for being with us, and I will let you begin. My pleasure, I'm happy to be here. As I mentioned, I am with Grunfeld Desiderio Leibowitz Silverman and Clayshot. We are an international trade firm in New York, headquartered in New York. We have offices throughout the country. We only do international...

Award-winning PDF software

Duty drawback time limit Form: What You Should Know

Exportation. Claim forms. Claims by persons on behalf of others; penalties for making fraudulent claims. Drawing down of drawing for certain types of goods. Importation of certain materials. 18 USC § 2515(b)(2), 19 USC § 2515(b)(10), and 18 USC § 2515A(b)(6) — Drawing from the United States. (b) Drawing from the United States—(1) A person claiming drawing from the United States under this section may choose to file an advance drawing claim from the date on which the goods were brought into the United States, subject to § 2515(b)(4) (e) (iii) (A), (B), (c), (d), or (e) (iii) (B). (2) A person claiming drawing from the United States under this section may elect to apply for an advance drawing claim from the date on which the goods were brought into the United States, subject to § 2515(b)(4) (e) (f), but may not make an election after the expiration of 6 months from the date the drawing application is filed. (3) A person claiming drawing from the United States under this section must show to the satisfaction of the CBP officer that the goods were produced primarily or wholly outside the United States in a country in which the United States imposes an appropriate duty on the production of a derivative. The drawing from the United States is exempt from duty if the goods were produced under the authority of, and for the purposes of trade as required under, the law of any country in which the person imported or produced the goods on January 18, 1990, for consumption or sale in the United States; or, if the goods were produced under the authority of, and for the purposes of trade as required under, the law of another country in which the person imported or produced the goods on January 18, 1990, for consumption or sale outside the United States. (4) Subparagraphs (1) and (2) do not apply with respect to goods made in any country in the world other than the United States. Drawback claim. A drawback claims under this subpart must be made to the U.S. Customs Service within 3 years after the date on which the item was imported into the United States by a person other than the United States. An advance drawing claim must be made to the U.S.

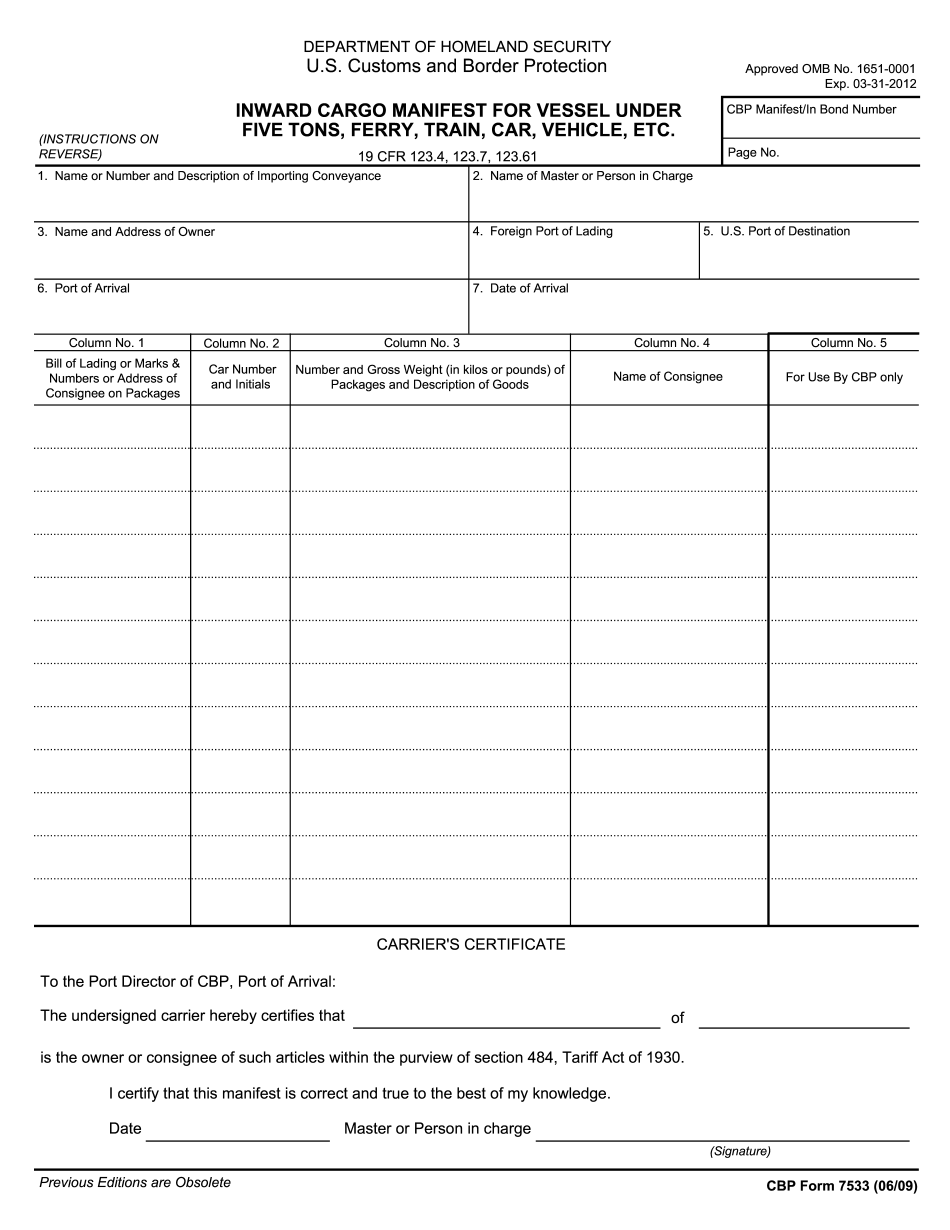

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Cbp Form 7533, steer clear of blunders along with furnish it in a timely manner:

How to complete any Cbp Form 7533 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Cbp Form 7533 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Cbp Form 7533 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Duty drawback time limit